The emergence of economic inequality as a public policy issue grew out of the wreckage of the Great Recession. And while it was protest movements like Occupy Wall Street that brought visibility to America’s glaring income gap, academic economists have had a near monopoly on diagnosing why it is that inequality has worsened in the decades since 1980.

Monopolies rarely deliver outstanding service, and this is no exception. The economics profession is fond of believing that its theorizing is an impartial, value-neutral endeavor. In actuality, mainstream (‘neoclassical’) economics is loaded with suppositions that have as much to do with ideology as with science.

Take the distribution of income, which economists argue is (in the final analysis) a consequence of production. Whether one earns $10 per hour or $10 million per year, the presumption is that individuals receive as income that which they contribute to societal output (their ‘marginal product’). In this vision, the free market is not only the best way to efficiently divide the economic pie, it also ensures distributive justice.

Get Evonomics in your inbox

But what if income inequality is shaped, in part, by broad power institutions—oligopolistic corporations and labor unions being two examples—such that some are able to claim a greater share of national income, not through superior productivity, but through market power?

In a study recently published with the Levy Economics Institute, I explore the power underpinnings of American income inequality over the past century. The key finding: corporate concentration exacerbates income inequality, while trade union power alleviates it.

Mass prosperity—the fabled ‘middle class’—was largely built between the 1940s and the 1970s. When President Roosevelt created the New Deal in 1935 union density was just eight percent. Density soared to nearly 30 percent by the mid-1950s, and the period spanning the 1930s to the 1970s would bear witness two major strike waves.

The combined effect was a surge in the national wage bill. In 1935 the share of national income going to the bottom 99 percent of the workforce was 44 percent. In tandem with strong unions and intense strike activity, the wage bill rose to 54 percent by the 1970s. In the period after 1980, union density and work stoppages both plummeted, pulling the wage bill down with them. American unionization is now just 11 percent and the wage bill sits at 41 percent—a seven decade-low for both metrics.

The declining power of the labor movement has many causes, but a series of state policies in the early 1980s hastened the demise. President Regan’s penchant for union busting and the crippling effects of overly restrictive monetary policy (the infamous ‘Volcker shock’) broke the back or organized labor. As trade union power declined, a crucial mechanism for progressively redistributing income began to fade in significance.

The decline of trade unions did not lead to an economic golden age, as some would have hoped. In the decades after 1980, business investment trended downward, job creation slowed and GDP growth decelerated—a phenomenon often referred to as ‘secular stagnation’. Many economists have wondered why, given business-friendly policies in Washington, investment declined so precipitously after 1980.

My study reveals that America does not suffer from a shortage of investment in the general sense. The American corporate sector has been spending more money than ever, but instead of ploughing resources into job creation and fixed asset investment, historically unprecedented resources are flowing into mergers and acquisitions (M&A) and stock repurchase, the combined effect of which has been slower growth and rising inequality (a finding which also applies to Canada—see here and here).

Unlike investment in fixed assets, which is linked with job creation, M&A merely redistributes corporate ownership claims between proprietors. The motivation for M&A is straightforward: large firms absorb the income stream of the firms they acquire while reducing competitive pressure, which increases their market power.

In the century spanning 1895 through 1990, for every dollar spent on fixed asset investment, American business spent an average of just 18 cents on M&A. In the period since 1990, for every dollar spent on fixed asset investment an average of 68 cents was spent on M&A—a four-fold increase.

The explosion of M&A since 1990 has led to the concentration of corporate assets (power, in other words). In 1990 the 100 largest American firms controlled 9 percent of total corporate assets. Asset concentration more than doubled over the next two decades, peaking at 21 percent. The creation of a concentrated market structure, which has gone largely unnoticed by the economics profession, is one reason inequality has worsened in recent decades.

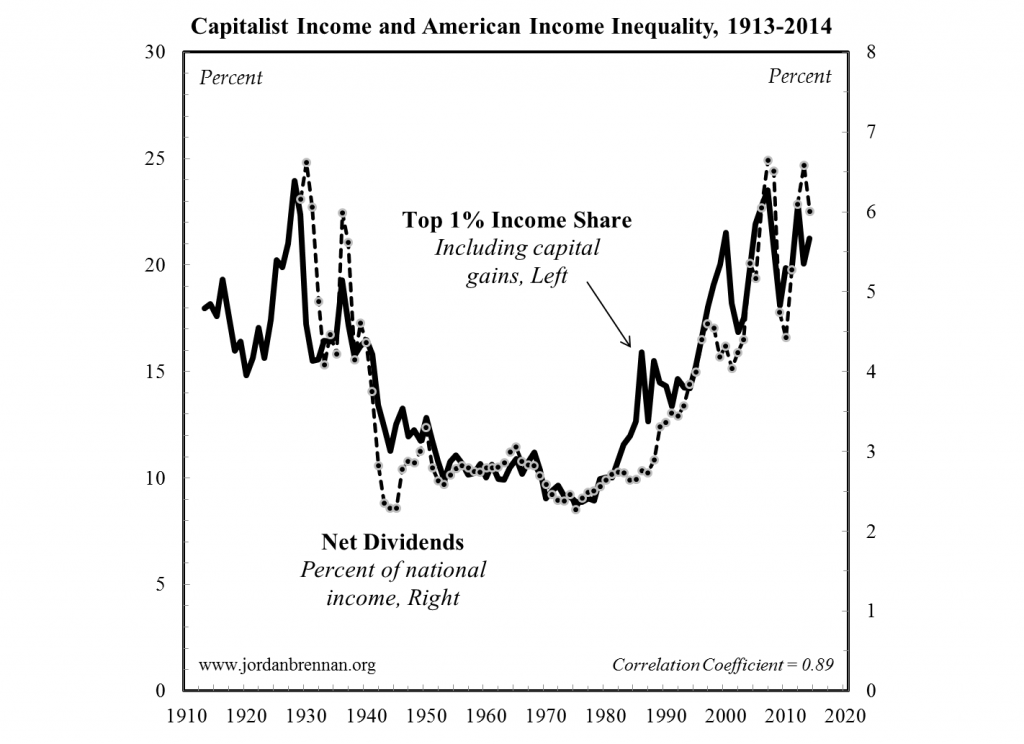

With more market power-generated income at their disposal, large firms have paid comparatively more to shareholders in the form of dividends (the enclosed figure contrasts the income share of the richest 1 percent of Americans with the dividend share of national income).

At the same time, the 100 largest firms have spent more repurchasing their own stock than they have on machinery and equipment. And because many executives have stock options in their contracts, the share price inflation associated with stock repurchase has led to soaring executive compensation.

It is in this manner that increasing corporate concentration has simultaneously slowed growth and exacerbated inequality. None of these developments are inevitable, but if we are to meaningfully confront the dual problem of secular stagnation and soaring inequality we must begin to understand the role that power plays in driving these trends.

2016 April 11

Donating = Changing Economics. And Changing the World.

Evonomics is free, it’s a labor of love, and it's an expense. We spend hundreds of hours and lots of dollars each month creating, curating, and promoting content that drives the next evolution of economics. If you're like us — if you think there’s a key leverage point here for making the world a better place — please consider donating. We’ll use your donation to deliver even more game-changing content, and to spread the word about that content to influential thinkers far and wide.

MONTHLY DONATION

$3 / month

$7 / month

$10 / month

$25 / month

You can also become a one-time patron with a single donation in any amount.

If you liked this article, you'll also like these other Evonomics articles...

BE INVOLVED

We welcome you to take part in the next evolution of economics. Sign up now to be kept in the loop!