April 2, 2016

The spectacular economic rise of the top 1 percent is now common knowledge, thanks in large part to the work of Thomas Piketty and his collaborators. The top 1 percent of U.S. residents now earn 21 percent of total national income, up from 10 percent in 1979.

Curbing this inequality requires a clear understanding of its causes. Three of the standard explanations—capital shares, skills, and technology—are myths. The real cause of elite inequality is the lack of open access and market competition in elite investment and labor markets. To bring the elite down to size, we need to make them compete.

Myth 1: Capital vs. labor share

In his recent and otherwise valuable book, Saving Capitalism: For the Many, not the Few, Robert Reich claims that the share of income going to workers has fallen from 50 percent in 1960 to 42 percent in 2012. Meanwhile, corporate profits have risen. In short: trillions of dollars have gone to capitalists instead of workers. The sensible policy responses, as Reich and others have stressed, are to increase taxes on corporate income and capital gains, and widen capital ownership.

These might be a good idea for other reasons, but the basic facts currently being used to justify them are wrong. Between 1980 and 2014, corporate profits actually represented alower share of GDP (4.9 percent) than between 1950 and 1979 (5.4 percent).

Income from the main four capital sources— dividends, interest, rental income, and proprietor income—has nudged upwards as a share of GDP by just one percentage point between these two periods, and entirely because of higher interest income, which mainly goes to retirees who own Treasury bonds.

Get Evonomics in your inbox

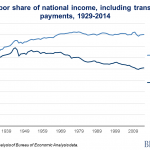

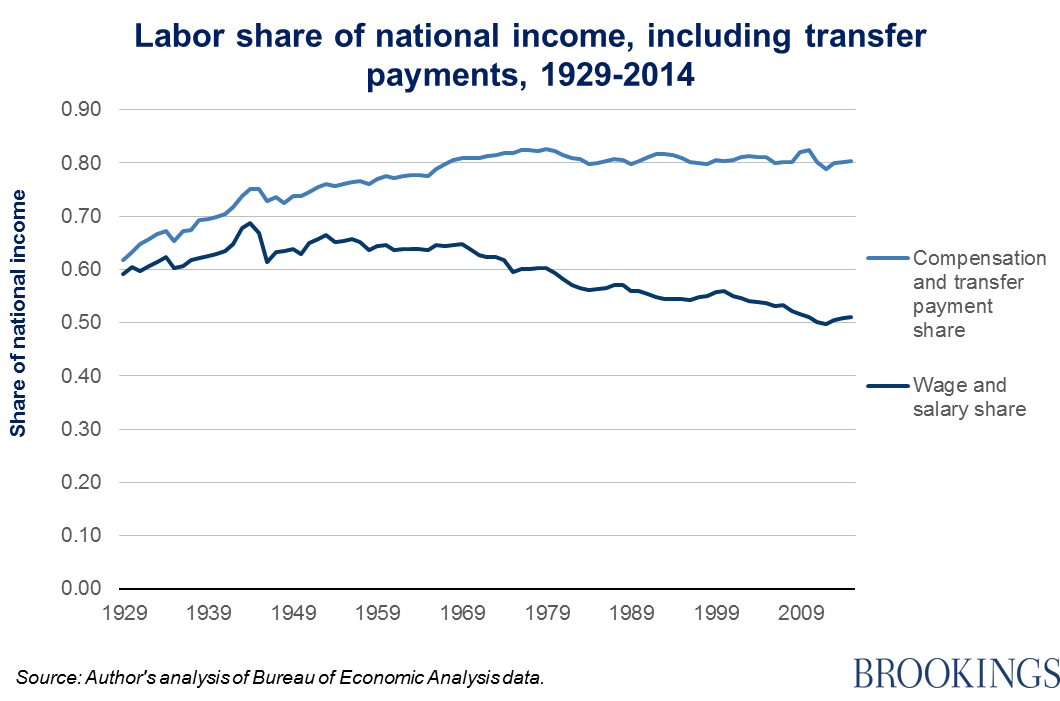

So, what’s going on here? The simple explanation is that wages and salaries are an inadequate measure of the share of economic benefits flowing to labor. Wages and salaries have declined as a share of total income, largely for two reasons. First, total national income includes government transfer payments, which are rising because of an aging population (e.g., Social Security and Medicare). Second, companies have greatly increased non-salary compensation (e.g., healthcare and retirement benefits). Total worker compensation plus transfer payments have actually slightly increased as a share of total national income, from 79 percent between 1951 and 1979, to 81 percent for the years from 1980 to 2015:

Myth 2: Super skills lead to super riches

In his “defense of the one percent,” economist Greg Mankiw argues that elite earnings are based on their higher levels of IQ, skills, and valuable contributions to the economy. The globally-integrated, technologically-powered economy has shifted so that very highly-talented people can generate very high incomes.

It is certainly true that rising relative returns to education have driven up inequality. But as I have written earlier, this is true among the bottom 99 percent. There is no evidence to support the idea that the top 1 percent consists mostly of people of “exceptional talent.” In fact, there is quite a bit of evidence to the contrary.

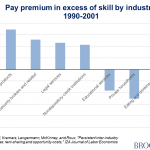

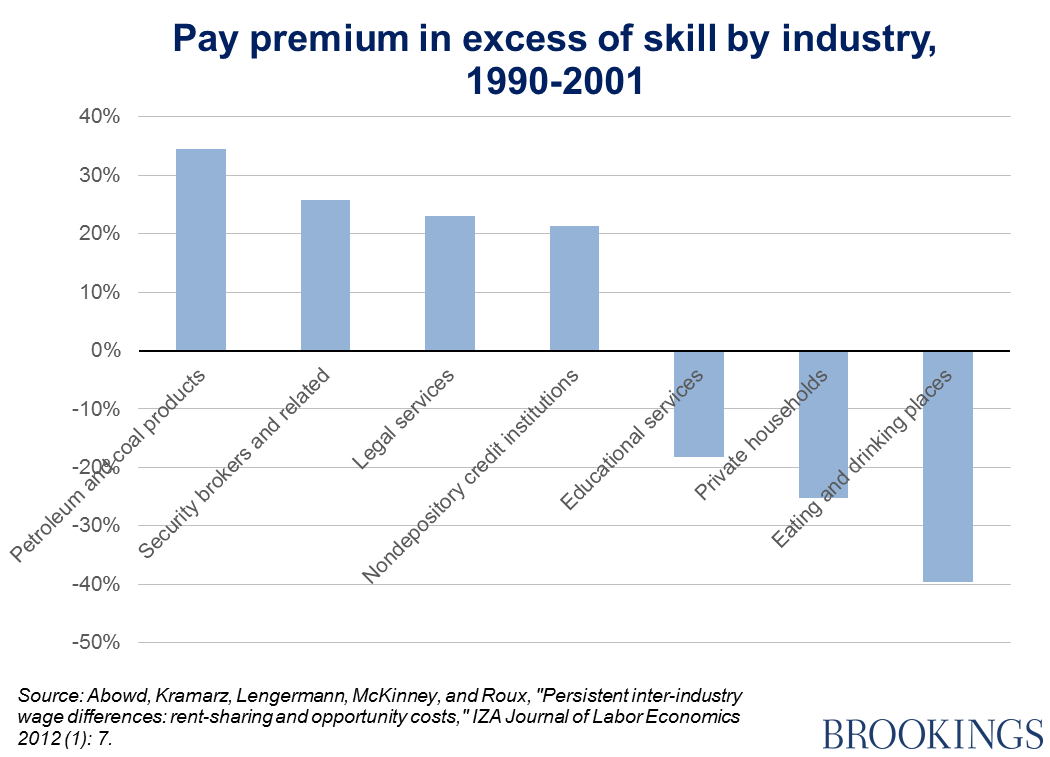

Drawing on state administrative records for millions of individual Americans and their employers from 1990 to 2011, John Abowd and co-authors have estimated how far individual skills influence earnings in particular industries. They find that people working in the securities industry (which includes investment banks and hedge funds) earn 26 percent more, regardless of skill. Those working in legal services get a 23 percent pay raise. These are among the two industries with the highest levels of “gratuitous pay”—pay in excess of skill (or “rents” in the economics literature). At the other end of the spectrum, people working in eating and drinking establishments earn 40 percent below their skill level.

Using data from an OECD cognitive test of thousands of Americans and adults from around the world (the PIACC), I find that workers in the financial and insurance sector get a pay bump equivalent to a decile of the earnings distribution (e.g., pushing them up from the 80thto 90th percentile). This is the largest premium aside from the quasi-monopolistic mining and utilities sectors:

At the occupational level, CEOs are paid 1.5 deciles above their “IQ.” Health professionals also receive a very large boost in earnings.

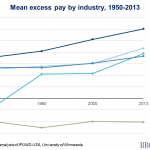

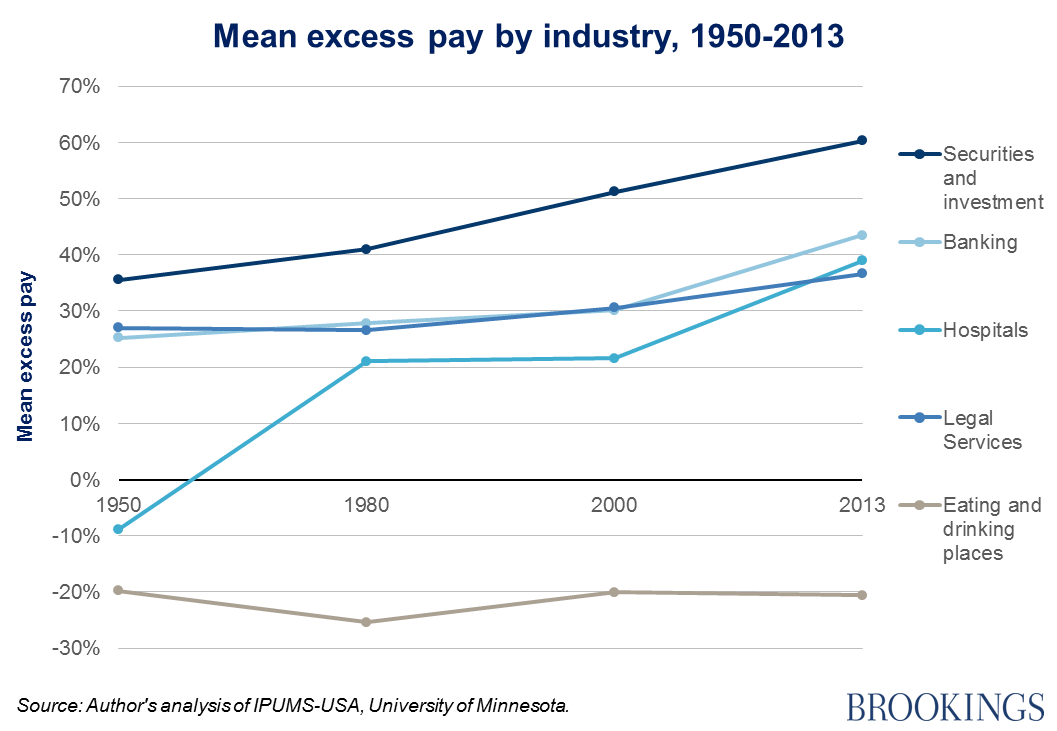

Using microdata from the Census Bureau, I find that the “gratuitous pay” premium in certain industries has increased dramatically since 1980. Workers in securities and investment saw their excess pay rise from 41 percent to 60 percent between 1980 and 2013. Legal services went from 27 percent to 37 percent. Hospitals went from 21 percent to 39 percent. Meanwhile, those working in eating and drinking establishments consistently hovered around negative 20 percent:

Myth 3: Technology

Some entrepreneurs grow enormously rich as a result of founding a company with an innovative product. This applies to Mark Zuckerberg, as well as to Bill Gates and other mega-stars of the tech sector. Venture capitalist Paul Graham has recently written about this as an important aspect of inequality, and he’s correct. It is. But again, it has little to do with the rise of the 1 percent.

Take some of the most important tech industries: software, internet publishing, data processing, hosting, computer systems design, scientific research and development, and computer and electronics manufacturing. Combined, they represent just 5 percent of workers in the top 1 percent of income earners.

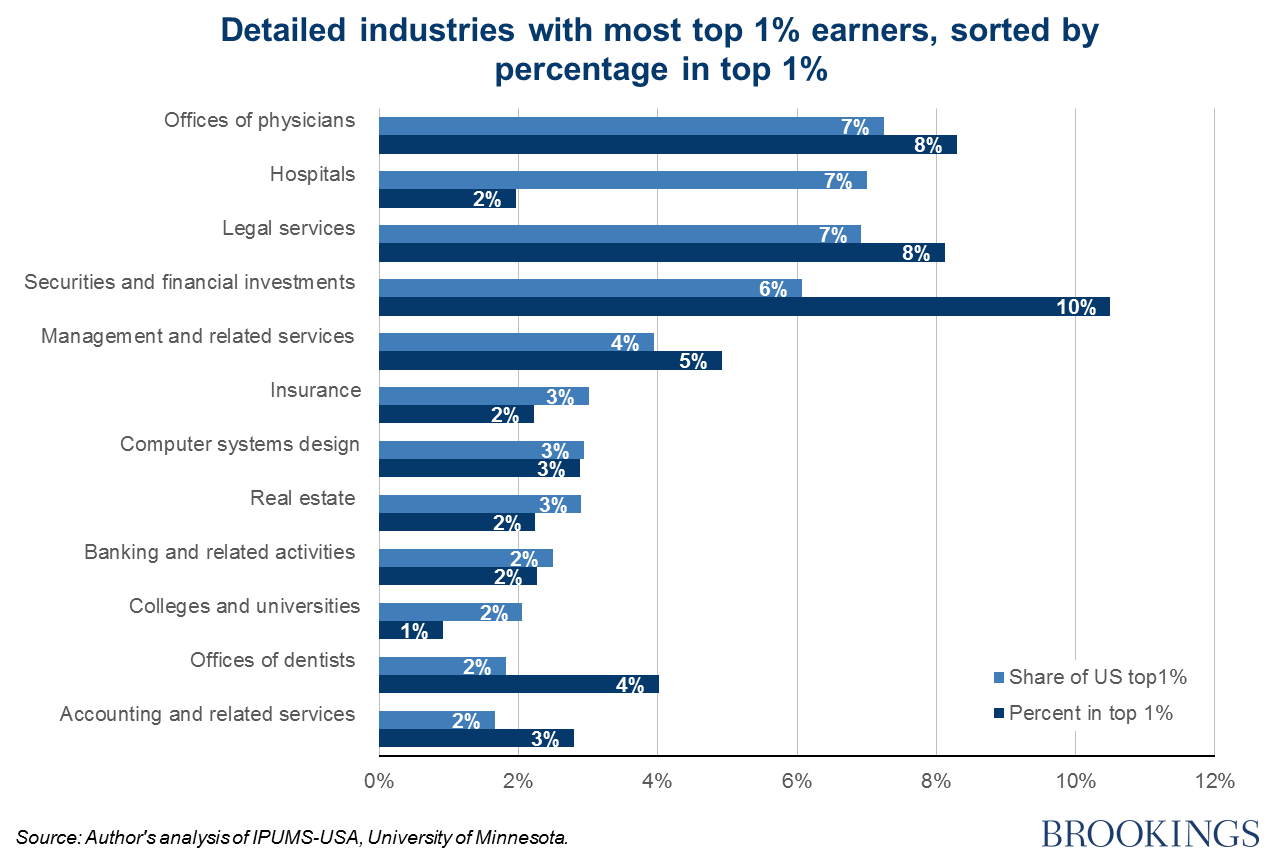

So, if they’re not in Silicon Valley making awesome stuff, where are the 1 percent working? Top answer: doctor’s offices. No industry has more top earners than physicians’ offices, with 7.2 percent. Hospitals are home to 7 percent. Legal services and securities and financial investments industries account for another 7 and 6 percent, respectively. Real estate, dentistry, and banking provide a large number, too:

Computer systems design is the only tech sector among the top contributors. There are five times as many top 1 percent workers in dental services as in software services.

CEOs are of course more likely to be in the top tier, especially if they are in certain privileged industries: 28 percent of CEOs from the financial sector, for instance, and 26 percent of those in hospitals. (But 15 percent of college presidents are in the top 1 percent, too.)

So if technology, skills, and capital shares can’t explain the rise of the top 1 percent, what does? And what can we do about it?

A non-elitist investment market

One way that the top 1 percent cements their position is by occupying the financial sector, and accessing above-market returns on their investments.

The large and growing prominence of the financial sector in terms of excess pay has a great deal to do with hedge funds, which barely existed before the 1980s but are now integrated into mainstream investment banks like Goldman Sachs and hold over a trillion dollars in assets from pension funds, university endowments, and other institutional and private investors.

A hedge fund is a loose term referring to an investment portfolio that is less regulated than other funds, because only very rich individuals or approved institutions (accredited investors or qualified purchasers) can participate in it. This regulatory distinction allows hedge funds to take more risk, borrowing levels of money that greatly exceed their assets (and avoid many onerous reporting requirements). These regulatory advantages have allowed hedge funds to consistently outperform stocks and other assets by roughly 2 percentage points each year.

The accredited investor rule has mostly been ignored by scholars of inequality. But legal scholars Houman Shadab, Usha Rodrigues, and Cary Martin Shelby are an exception. They have each written persuasively about how the rules contribute to inequality by giving the richest investors privileged access to the best investment strategies. Shadab points out that other countries (with less inequality) allow retail investors to access hedge funds.

The law has also inflated the compensation of hedge fund workers—roughly $500,000 on average—by restricting competition. Mutual funds—which charge tiny fees by comparison—are currently barred from using hedge fund strategies because they have non-rich investors. If the law was changed to allow mutual funds to offer hedge fund portfolios, hundreds of billions of dollars would be transferred annually from super-rich hedge fund managers and investment bankers to ordinary investors, and even low-income workers with retirement plans. A House committee recently approved a bill that would slightly ease the accredited investor rule. Even if it became law, the bill would be a modest step—but at least one in the right direction.

A non-elitist labor market

At the same time, we need more competition at the top end of the labor market. As economist Dean Baker points out, politicians and intellectuals often champion market competition—but what they mean by that is competition among low-paid service workers, production workers, or computer programmers who face competition from trade and immigration, while elite professionals sit behind a protectionist wall. Workers in occupations with no higher educational requirements see their wages held down by millions of other Americans denied a high-quality education and competing for relatively precious vacancies.

For lawyers, doctors, and dentists— three of the most over-represented occupations in the top 1 percent—state-level lobbying from professional associations has blocked efforts to expand the supply of qualified workers who could do many of the “professional” job tasks for less pay. Here are three illustrations:

- The most common legal functions—including document preparation—could be performed by licensed legal technicians rather than lawyers, as the Washington State Supreme Court decided in 2012. These workers could perform most lawyer-like tasks for roughly half the cost. Unsurprisingly, legal groups opposed it. A few brave souls from the Washington State Bar Association board resigned in protest, and issued this statement: “The Washington State Bar Association has a long record of opposing efforts that threaten to undermine its monopoly on the delivery of legal services.” Proportion of lawyers in the top 1 percent? 15 percent.

- Many states allow nurse practitioners to independently provide general and family medical services, freeing up physicians to provide more specialized services. But most larger states do not. Again, typical nurse practitioner salaries are roughly half those of general practitioners with an MD. But, of course, physician lobbies stridently oppose the idea. Proportion of physicians and surgeons in the top 1 percent? 31 percent.

- Dental hygienists can perform many of the functions of more far expensive dentists, but regulations vary by state and in all but a few states, it is not possible for hygienists to own and operate their own practice. My analysis shows that just 2 percent of hygienists are self-employed compared to 63 percent of dentists. Proportion of dentists in the top 1 percent? 21 percent.

Recently, the head of the Federal Trade Commission testified before the U.S. Senate on how state occupational licenses, such as these, often hinder competition and harm consumers, though her agency has very little authority to intervene.

Less Karl Marx, more Adam Smith

The modern left still too often sees the world through a Marxist lens of capitalist owners trying to exploit people who sell their labor for a living. But that doesn’t help explain rising top incomes. On the other hand, many on the modern right wrongly infer that great earnings must only be generated by great people.

Progressive thinkers tend to revert to an anti-market stance, which means they reach for the wrong solutions in terms of policy. Conservatives, meanwhile, are often keen to remove regulatory barriers to competition, but still defend the financial sector and other elite earners.

Before Marx, Adam Smith provided a framework for political economy that is especially useful today. Smith warned against local trade associations which were inevitably conspiring “against the public…to raise prices,” and “restraining the competition in some employments to a smaller number than would otherwise…occasion a very important inequality” between occupations.

For earnings to be distributed more fairly, our goal is not to stand in the way of markets, but to make them work better.

Originally published here.

2016 April 2

Donating = Changing Economics. And Changing the World.

Evonomics is free, it’s a labor of love, and it's an expense. We spend hundreds of hours and lots of dollars each month creating, curating, and promoting content that drives the next evolution of economics. If you're like us — if you think there’s a key leverage point here for making the world a better place — please consider donating. We’ll use your donation to deliver even more game-changing content, and to spread the word about that content to influential thinkers far and wide.

MONTHLY DONATION

$3 / month

$7 / month

$10 / month

$25 / month

You can also become a one-time patron with a single donation in any amount.

If you liked this article, you'll also like these other Evonomics articles...

BE INVOLVED

We welcome you to take part in the next evolution of economics. Sign up now to be kept in the loop!